DUI Auto Insurance: What It Is, Costs, and How to Find Coverage

If you have been convicted of driving under the influence, getting car insurance can become more difficult. DUI auto insurance refers to coverage for drivers who have a DUI on their record and are therefore considered higher risk by insurance companies. Because of this classification, drivers often face higher premiums, fewer insurer options, and additional requirements such as filing an SR-22 or FR-44 form.

Even with these restrictions, drivers can still obtain coverage. In this post, you’ll learn how DUI auto insurance works, what affects the price, and where to look for policies that can help you meet legal requirements and find insurance that fits your situation.

What Is DUI Auto Insurance?

DUI auto insurance refers to car insurance coverage for drivers who have been convicted of driving under the influence of alcohol or drugs. The policy itself is not different from standard auto insurance, but insurers classify these drivers as high risk, which affects pricing and eligibility.

After a DUI, insurance companies evaluate your record more closely. Most insurers review your Motor Vehicle Report (MVR) to identify serious violations and determine how likely you are to file a future claim.

Because of that risk assessment, DUI auto insurance usually involves:

- Higher premiums compared to drivers with clean records

- Fewer insurers are willing to offer coverage

- Additional state requirements, such as filing an SR-22 or FR-44 form

These filings are not a type of insurance. They simply prove to the state that you maintain the minimum liability coverage required to legally drive.

The stricter approach from insurers is tied to real safety risks. According to the National Highway Traffic Safety Administration (NHTSA), alcohol-impaired driving accounted for about 32 percent of all traffic fatalities in the United States in 2022. This elevated risk is one reason insurance companies adjust premiums after a DUI conviction.

How a DUI Affects Your Car Insurance

A DUI conviction has a direct impact on how insurance companies evaluate your driving risk. In most cases, it leads to higher premiums, stricter policy conditions, and fewer insurer options.

Here are the most common ways a DUI affects your car insurance.

Higher Insurance Premiums

Insurance companies calculate premiums based on risk. A DUI signals a higher probability of accidents or future claims, which usually leads to a significant price increase.

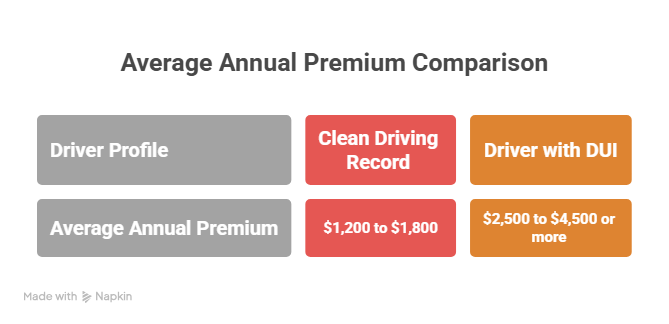

Many drivers see their premiums rise by 50 percent to more than 100 percent after a DUI. According to research from Insurance.com, the average increase nationwide is about 74 percent.

Example

- Before DUI: about $1,500 per year

- After DUI: $2,600 or more per year

The exact increase depends on factors such as your state, insurer, driving history, and age.

Possible Policy Cancellation or Non Renewal

Some insurance companies choose not to continue coverage after a serious violation.

This can happen in two ways:

- Policy cancellation, where the insurer ends the policy before the renewal date

- Non renewal, where the company refuses to renew the policy at the end of the term

If this happens, you will need to look for another insurer that accepts high risk drivers.

SR-22 or FR-44 Requirements

Many states require drivers with a DUI to file proof of financial responsibility.

The most common filings include:

- SR-22, required in many states after serious violations

- FR-44, used in states such as Florida and Virginia and usually requires higher liability limits

These documents confirm that you maintain the minimum insurance required by law. Drivers typically must keep them on file for three to five years, depending on state regulations.

How Much DUI Auto Insurance Costs

The cost of DUI auto insurance varies widely, but most drivers pay more after a DUI conviction. Insurance companies increase premiums because drivers with serious violations are considered higher risk.

On average, drivers with a DUI pay thousands of dollars more per year compared to drivers with clean records.

Factors That Affect DUI Insurance Prices

Several factors influence how much you will pay for DUI auto insurance.

- State laws and regulations

- Your age and driving history

- Type of vehicle you drive

- Coverage limits and deductible

- Insurance company risk policies

For example, a driver with multiple violations or accidents will typically pay more than someone whose DUI is their first major offence.

Because pricing varies significantly between insurers, many drivers find lower rates by comparing quotes from several companies.

How to Get Car Insurance After a DUI

Finding car insurance after a DUI may take more effort, but most drivers can still obtain coverage. The key is understanding where to look and how insurers evaluate high-risk applicants.

Many large insurance companies still provide policies to drivers with a DUI, although premiums are usually higher. Some of the insurers commonly known for covering higher-risk drivers include:

- Progressive

- GEICO

- State Farm

- Dairyland

Each company evaluates risk differently, which means prices can vary significantly. Comparing several quotes is often the best way to identify a more affordable option.

If traditional insurers decline your application, another possibility is a state-assigned risk pool. These programs are designed for drivers who cannot obtain coverage in the regular insurance market. While premiums are typically higher, they allow drivers to meet the legal requirement to carry insurance.

When applying for DUI auto insurance, insurers usually review several factors, including:

- Your Motor Vehicle Report

- The number of violations on your record

- How recent the DUI conviction is

- Whether you must file an SR-22 or FR-44

Drivers who maintain a clean record after the conviction often find that insurance options improve over time as their risk profile changes.

How to Lower Your DUI Auto Insurance Costs

Although DUI auto insurance is usually more expensive, there are several ways drivers can gradually reduce their premiums over time. Insurance companies reassess risk regularly, so responsible driving and smart policy choices can make a difference.

1. Compare Quotes From Multiple Insurers

Insurance rates for high-risk drivers vary widely between companies. Comparing quotes from several insurers can reveal significant price differences for the same level of coverage.

Many drivers compare at least three to five insurers before choosing a policy.

2. Take Defensive Driving or Education Programs

Some insurers offer discounts for drivers who complete:

- defensive driving courses

- DUI education programs

- traffic safety training

These programs show insurers that the driver is taking steps to reduce risk.

3. Maintain a Clean Driving Record

Avoiding additional violations is one of the most important factors in lowering insurance costs.

Over time, a record without new tickets or accidents helps insurers reassess the driver's risk level.

4. Adjust Your Coverage and Deductible

Another way to manage costs is by reviewing policy details. For example:

- Choosing a higher deductible can lower monthly premiums

- Adjusting coverage levels may reduce overall policy costs

Many drivers see premiums gradually decrease after several years without additional violations.

Find DUI Auto Insurance with Mila

A DUI conviction can make car insurance more expensive and limit the number of insurers willing to offer coverage. Even so, drivers can still find policies that meet legal requirements and gradually improve their insurance profile over time.

Comparing quotes from multiple insurers is often the most effective way to identify better rates and coverage options. With Mila, you can compare real-time quotes from top providers in one place, making it easier to review policies, choose the right coverage, and move forward with confidence.

Get real-time quotes from top providers with Mila. Compare, choose, and save all in seconds.

Frequently Asked Questions (FAQs) About DUI Auto Insurance

Can you get car insurance after a DUI?

Yes. Most drivers can still obtain car insurance after a DUI conviction. However, insurers usually classify these drivers as high risk, which means premiums are typically higher and coverage options may be more limited.

How long does a DUI affect insurance rates?

A DUI can affect insurance rates for several years. In many states, insurers consider a DUI violation when calculating premiums for three to ten years, depending on state regulations and company policies.

Which insurance companies insure drivers with a DUI?

Many large insurers still provide coverage for drivers with a DUI. Companies often mentioned for higher risk drivers include Progressive, GEICO, State Farm, and Dairyland. Availability and pricing depend on the state and the driver's history.

What is the best way to find DUI auto insurance options?

The most effective way is to compare quotes from multiple insurers. Rates for drivers with a DUI can vary significantly between companies. Using a comparison platform like Mila allows you to review real-time quotes from several providers and choose coverage that fits your situation.